Bullets:

Countries and firms are borrowing billions of dollars by accessing China’s debt markets, which offer some of the lowest interest rates in the world.

Panda Bonds are available to some borrowers of Chinese renminbi, to finance business operations in Mainland China, even by banks and companies outside China.

Chinese regulators maintain strict safeguards on who can borrow and use RMB abroad, and for what purposes.

Companies are swapping US Dollar-denominated debt for Chinese capital, and cutting borrowing costs by over half, while reducing FX volatility and and eliminating risks of sanction and asset seizure.

Inside China / Business is a reader-supported publication. To receive new posts and support my work, consider becoming a free or paid subscriber.

Report:

Good morning.

Countries and companies are shifting away from the US dollar, and from the Western banks. And the process is accelerating.

The demand for an alternative system was always there, but the plumbing was not. That’s to say that new networks had to be established and tested. Bilateral trade agreements, outside the US dollar and European banks, were set up and today are growing fast. New commodities exchanges needed to be set up, with regulations and procedures for those new trading systems.

Now we’re seeing strong demand to borrow Chinese renminbi, instead of US dollars or euro, by major bond market issuers. Countries are borrowing renminbi to pay higher-cost US-dollar denominated debt, and here we can see why.

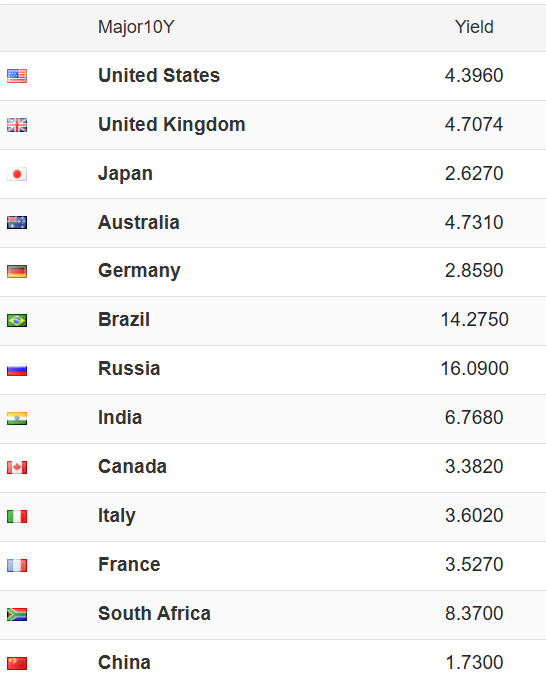

These are the 10-year government bond yields. The US Treasury borrows for 4.39% for ten years; it follows that companies borrowing US dollars in capital markets, or from banks, pay higher rates that the American government does.

Japan had a zero-interest rate policy until recently; now they’re at 2.6% and companies borrowing yen are paying over 4% coupons for new money. But the outlier on that chart is China, at just 1.73%. So companies are borrowing in Chinese renminbi, to repay loans denominated in other currencies. And other companies are borrowing RMB to refinance loans that are maturing, and which need to be rolled over at new, higher rates than when first issued.

The problem for most would-be borrowers is that China’s capital markets are not open to everyone. Chinese regulators protect their currency from speculators. And the renminbi is not a source of capital for Wall Street traders using low-cost foreign money to do carry trade operations, as they did for years with the Japanese yen.

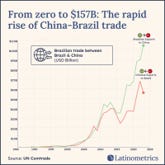

It is, however, a strong alternative for companies that do real trade, and real business with China. Brazil is a fellow BRICS member and a major trading partner with China, and its central bank is issuing Panda bonds for the first time.

And there we see who Panda bonds are for. Companies in Brazil asked the government there to create capital pools in RMB, so those firms can more easily borrow in RMB, in Brazil and here. Using RMB will reduce the interest rate and FX volatility, and their overall costs. Brazil’s mines and farms do massive trade with China, and need more renminbi in banks there to expand. That all comports with what Beijing wants to do anyway: deepening trade relationships using renminbi, while keeping guardrails up on who is allowed to borrow and use the Chinese currency outside China.

Emerging markets like Brazil are naturally seeking alternatives outside the US dollar. And the booming trade in Brazilian soybeans and Brazilian crude oil, for example, needs to be completely outside the US dollar and the European SWIFT system to insulate that trade from threat of sanctions, or asset seizures.

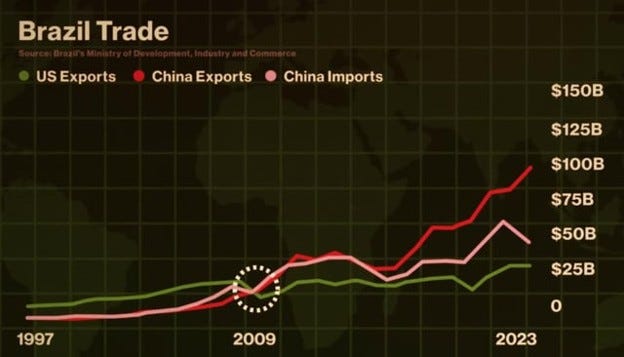

Brazil has the 10th largest economy in the world, and trade between Brazil and China went from “does not exist” twenty years ago to one of the biggest bilateral trading relationships in the world.

In 2009, Brazil’s exports to the United States and China were roughly the same; fifteen years later Brazil’s exports to China were four times higher than to the US. That means that Brazilian companies were doing business with China, but in USD, and are desperate to get away from high-cost US dollars and US banks to make this trade go, and telling their government officials in Brazil to get them a better way to do that business.

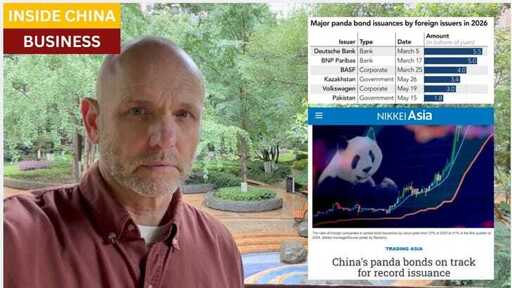

Pandas are bonds denominated in the Chinese currency, and issued here, in China, by institutions outside China. Those borrowers include Chinese owned-companies across the world, and foreign companies that do business here in China. Also, “sovereign entities”—central banks, in Brazil’s case, who have Brazilian companies who need access to Chinese renminbi. Panda bonds have been around for over 20 years, but demand is booming because of high interest rates everywhere else, geopolitical problems, and Chinese regulators opening up their debt markets to new borrowers.

Foreign institutions are using the renminbi as long-term funding vehicles, and central banks are holding more RMB in the FX reserves, and for their domestic companies to expand trade with China.

Companies who can access new capital at low rates have an advantage, over companies who cannot. Cost of capital is a major driver of competitiveness, and we have this weird situation now: companies who are doing trade with China, and who can borrow in RMB, can borrow at lower rates than even their own governments. Fortescue is an Australian mining company, and last year borrowed 14 billion RMB – that’s $2.1 billion US – at 3.8% a year. That’s almost a full point lower than the Australian government itself can borrow. The Australian government is a sovereign issuer of debt, and can raise taxes to pay that debt, or just print money. But an Australian company doing lots of business with China borrows at lower rates than the Australian government.

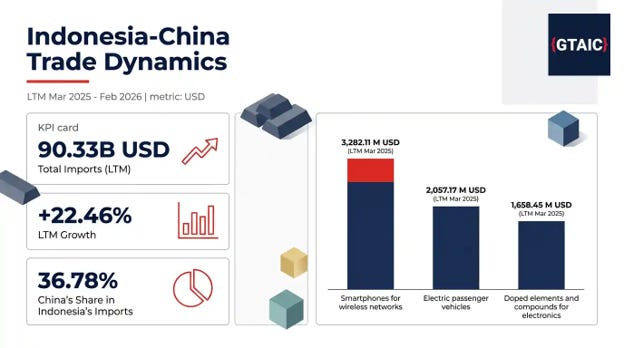

Indonesia is another BRICS country, and another that does a lot of business with China. They, too, are hitting Panda markets to finance growth. The Indonesian economy is booming; GDP growth over 5%, and trade with China is up over 22% over the trailing 12 months.

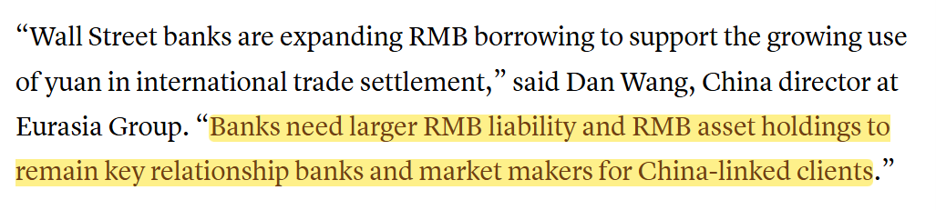

Global companies everywhere need low-cost capital to grow, and Wall Street and European banks have a big problem if other banks can borrow and lend in RMB, while they cannot. Morgan Stanley and Deutsche Bank are raising billions of RMB at rates below 3%, which is far less than they can borrow in USD or Euro. These are too-big-to-fail banks in the US and Europe, yet even they need to be active in China’s Panda bond markets to have any chance of keeping their bank customers who do business with China. That’s the thinking of most of these financial institutions; banks are more active now in the Panda bond markets than governments and large companies, for that reason.

So now issuance of these bonds is hitting records, rising twice as fast as last year. In Q1 of 2026, issuance was already two-thirds of all of 2025. Panda bonds are more difficult to issue than Dim Sum bonds, and Panda’s are not actively traded in secondary markets. That’s to say again that Panda’s are lousy for speculators or active traders. They’re held to maturity by borrowers.

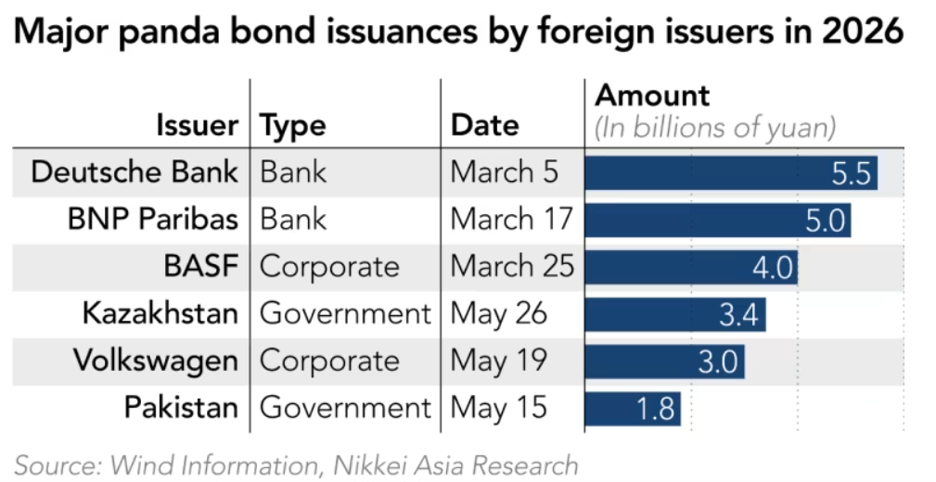

Besides banks and governments, companies are accessing Chinese bond markets directly, to fund their operations here. BASF is shutting down facilities in Europe, and expanding operations in China, and doing so with low-cost capital from Chinese debt markets. Same thing is going on at VW.

Everything costs more in Europe, compared to China. Even the money.

Be good.

Resources and links:

Resources and links:

Fast-growing panda bond market helping repay US dollar debt

https://www.financeasia.com/article/fast-growing-panda-bond-market-helping-repay-us-dollar-debt/507620

Yuan Bonds Boom as Borrowers Shift Away From U.S. Dollar Funding

https://www.caixinglobal.com/2026-04-10/yuan-bonds-boom-as-borrowers-shift-away-from-us-dollar-funding-102432518.html

Global government bond yields, 10-year

https://tradingeconomics.com/bonds

Brazil plans largest panda bond debut to ‘test’ waters

https://www.reuters.com/world/americas/brazil-plans-up-5-billion-yuan-panda-bond-issuance-says-finance-minister-2026-06-25/

Brazil to issue first sovereign panda bonds in Latin America

https://www.globaltimes.cn/page/202606/1364484.shtml

Indonesia’s Panda Bond issuance remains on track for early July

https://en.antaranews.com/news/420500/indonesias-panda-bond-issuance-remains-on-track-for-early-july

Panda Bonds explained: understanding China’s growing bond market

https://www.db.com/news/detail/20250228-panda-bonds-explained-understanding-china-s-growing-bond-market?language\_id=1

Why Wall Street banks and foreign borrowers are rushing to tap China’s cheap money

https://www.cnbc.com/2026/06/18/china-panda-bonds-yuan-funding-costs-foreign-borrowers.html

The panda bonds: how China uses assets to boost yuan’s profile, cement partnerships

https://www.scmp.com/business/banking-finance/article/3357883/panda-bonds-how-china-uses-assets-boost-yuans-profile-cement-partnerships

China’s panda bonds on track for record issuance

https://asia.nikkei.com/business/markets/trading-asia/china-s-panda-bonds-on-track-for-record-issuance

Overview of the Opening up of China’s Bond Market and Panda Bond Market

https://www.icmagroup.org/assets/documents/About-ICMA/APAC/NAFMII-and-ICMA-English-version-PANDA-BONDS-Raising-Finance-in-Chinas-Bond-Market-case-studies-September-2021-021121.pdf

Indonesia-China Trade Surges to 90.33 Billion USD in LTM Mar 2025 - Feb 2026

https://gtaic.ai/trends/indonesia-china-trade-report-ltm-mar-2025-feb-2026

Indonesia posts fastest economic growth rate in three years

https://www.reuters.com/world/asia-pacific/indonesia-q4-gdp-growth-beats-forecast-highest-since-2022-2026-02-05/

How Australia’s mining giants are helping China to globalise the yuan

https://www.scmp.com/economy/china-economy/article/3353274/how-australias-mining-giants-are-helping-china-globalise-yuan

China pushes to de-dollarize commodities markets, sets up new metals exchange

The BRICS trading system is already wiping out US farmers, as global price discovery is destroyed

The Japan Carry Trade Unwinding

https://blog.marketresearch.com/the-japan-carry-trade-unwinding

De-dollarization in Australia

BASF to exit hydrosulfites business and close production facility in Ludwigshafen

https://www.basf.com/global/en/media/news-releases/2025/09/p-25-181

Volkswagen to Cut 100,000 Jobs and Close Four Plants: Report

https://eletric-vehicles.com/vw-group/volkswagen-to-cut-100000-jobs-and-close-four-plants-report/

VW Group speeds up production cycle with ‘In China, for China’ strategy

https://www.automotivelogistics.media/supply-chain/vw-group-speeds-up-production-cycle-with-in-china-for-china-strategy/2629663

Inside China / Business is a reader-supported publication. To receive new posts and support my work, consider becoming a free or paid subscriber.

From Inside China / Business via This RSS Feed.