Bullets:

Order backlogs for new jets will take over a decade to clear, as Airbus and Boeing cannot build or deliver planes on time.

As a result, airlines are flying older planes for far longer than they had planned.

Older planes are more expensive to maintain, and are less fuel efficient than new aircraft.

Jet price prices are soaring higher, doubling in major markets from a year ago, while the industry had forecast a drop in oil and fuel prices for 2026.

COMAC is a Chinese aircraft manufacturer and is quickly scaling up production, but not yet fast enough to meaningfully close the gap between new plane demand, and production from the duopoly of Boeing and Airbus.

Inside China / Business is a reader-supported publication. To receive new posts and support my work, consider becoming a free or paid subscriber.

Report:

Good morning.

COMAC is a Chinese airplane manufacturer, which builds the C919. And Chinese airlines have a major problem, which is shared by all airlines, everywhere in the world: their planes are getting older, faster than they can be replaced.

Aircraft replacements are still below the levels of the previous decade: current deliveries are behind the rates of 2019. And since 2020, the number of planes over 20 years old is growing faster than new aircraft rolling off the lines.

Older planes means that airlines spend more money to keep them flying. All the costs go up. They need to be more closely inspected, maintenance and repairs go up, which means higher costs for replacement parts, and the technicians. And older planes are less fuel efficient. It’s especially a problem for the most expensive parts, like engines and landing gear assemblies.

So COMAC sees an opportunity, especially in China, to grab market share from Boeing and Airbus. And China overall represents the fastest-growing aviation market in the world. It will be the biggest market. India and Indonesia will also be major markets here in East Asia:

And the problem with aircraft availability is global, and urgent. It’s the most significant constraint to the growth across all the markets: airlines are ordering planes, but airline manufacturers cannot build and deliver them.

This is the industry update and forecast from last December, from the International Air Transport Association. Severe supply chain problems constrain the ability of airlines to grow new markets, and even to meet their demand for replacement jets. The backlog in aircraft orders is growing, and accelerating, and those same supply chain issues are impacting existing fleets and are a “drag on airline profitability.”

That’s to say that the same supply chain problems that preclude Boeing and Airbus from building new planes, also mean that replacement parts are hard to come by. Production is picking up some, compared to before, but new orders are coming in even faster, so the backlogs grow.

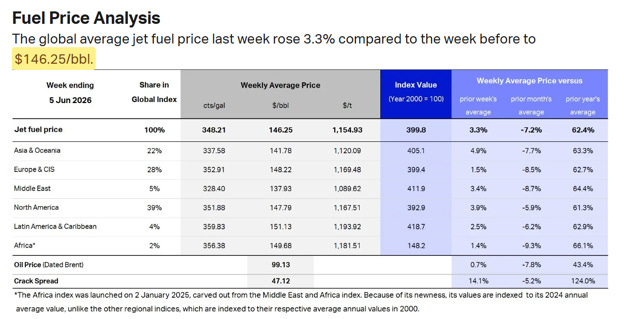

The IATA has a breakdown of the industry’s cost structures. Remember, this is from December, 2025. But things are already much worse than they thought. The industry forecast for 2026 called for a decline in fuel costs, with a consensus view for crude oil to be $62 a barrel, and jet fuel costs to drop to $88 a barrel. Fuel will be 25.7% of airlines’ operating expenses in 2026, a percent below the previous year.

We all know that didn’t work out, but here’s how much they were off: the cost for jet fuel is $146.25 a barrel, and higher in the North American and European markets:

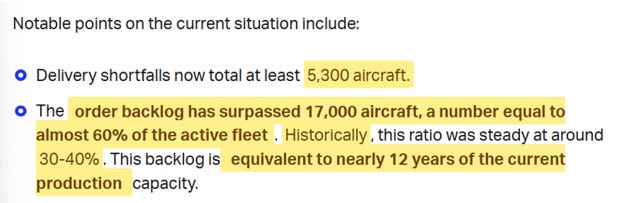

We’ll return later to the fuel problem. The demand for new aircraft, compared to new production, is only worsening, and the mismatch isn’t going to go away until the 2030’s. There is a record-high order backlog of over 17,000 planes:

That is 60% of the active fleet, right now. Historically, the ratio was half that. This industry wants to grow, and has placed orders, but manufacturers cannot keep up. They need 12 years of current production capacity just to meet the backlog they had, last December. There are over 5,000 planes in storage, but those need new parts and new certifications, and those are harder to get.

So old planes are flying for longer, and airlines are flying the wrong kinds of planes in many markets.

Most of the delays are supply-chain related. Engine manufacturers, for example, cannot keep up with production of the airframes, which are being parked until the engines get finished and installed.

Tariffs blew up supply chains last year. Tariffs on China, Canada, and the EU slowed everything down and drove costs up. Add up all the new costs that were hitting airlines—before the war on Iran—and it’s over $10 billion a year. These all result from that order backlog of 17,000 planes, and airlines flying older jets for longer.

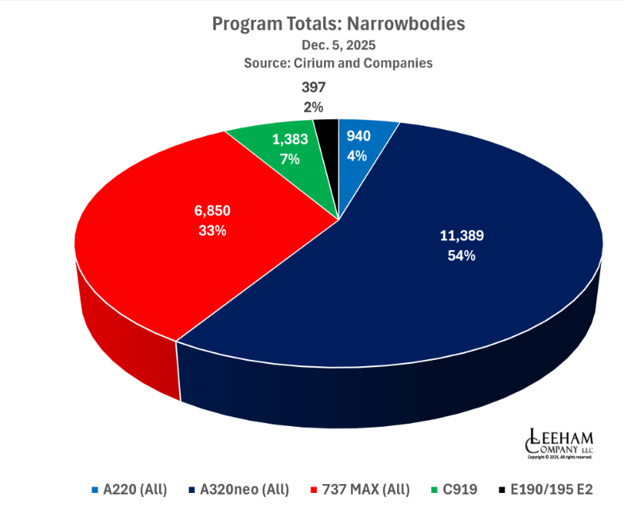

A key problem for the airline industry is this duopoly; Boeing and Airbus have 90% of the market share. This chart is for narrowbody jets, which include the C919. COMAC and Embraer combine for only 9% of this market.

Russia also builds narrowbody jets, but their companies are under sanction, and that is another big part of the problem. Russia is the primary source for titanium to Airbus and Boeing and the engine makers, and those companies now need special waivers to buy Russian titanium. The price is shooting higher. There are also shortages in aluminum and steel.

And civilian airlines are trying to buy new planes at the same time the Pentagon and other governments are racing to build new military aircraft. “Military programs compete aggressively with commercial aviation for an acutely limited labor pool”.

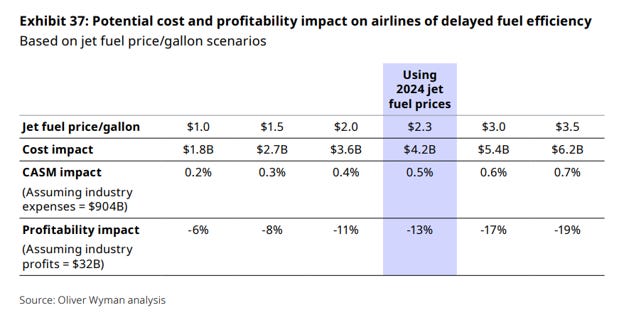

So everything is tight—supply chain constraints are everywhere, and costs are going up. Back to the fuel cost efficiency problems, when flying older planes. This table shows the impact on profitability at different price points for jet fuel. Remember, the industry experts believed that fuel prices would drop to 2024 levels, in 2026, and that would be a $32 billion dollar hit to industry profitability.

That was based on a jet fuel price of $2.30 a gallon. Top line. But today it’s over twice that. In the US, jet fuel is over $7 per gallon at major airports.

The cost of flying all those older planes drives airlines’ fuel costs up, even in peacetime. Then come the higher maintenance costs on the older aircraft. The average plane today is two years older than the ones flying in 2019. Maintenance has to be performed more often, and become more complex. More inspections for issues such as metal fatigue and stress fractures in the airframes, for example. More planes need to be overhauled and retrofit completely, which further strains the supply chains for parts, and on skilled labor.

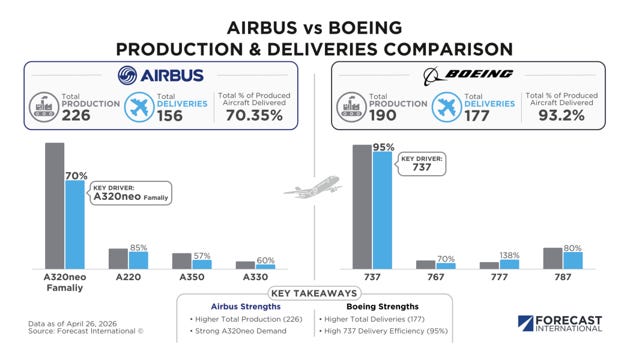

And Airbus and Boeing cannot keep up with deliveries for new planes. Airbus had previously been meeting their delivery schedules better than Boeing, but now Airbus can’t get engines fast enough to meet their delivery schedules.

Boeing, Airbus, and Pratt & Whitney all use a just-in-time inventory management system, which is failing in practice as well as in theory—JIT means that production happens as new orders come in: that is when parts are ordered and work begins, to meet demand. But the demand is there, and the production is not. So Pratt can’t build engines, so Airbus can’t deliver planes.

And making it all worse is that the airlines need to keep their old planes flying with old engines, which in turn need replacement parts to make that go. Everyone is blaming everyone else, and we’re back to the duopoly and monopolies: there are too few manufacturers, and a tiny group of companies are happy with the way things are right now. Backlogs are a big problem for airlines, but an opportunity for Pratt & Whitney to make money selling new engines to Airbus, as well as old ones to the airlines—at high prices, and there’s nothing that the airlines or Airbus can do about it.

So this is where we are. This is as of 30 April, so 4 months in to 2026. Airbus production—not deliveries, but production—was 226 planes. At Boeing it was 190. A smaller number actually were delivered, so let’s just look at best case. 226 plus 190 is 416. Divided by 4 months is 104 planes. At 104 planes per month, it will take 159 months, or over 13 years, to clear that backlog of 17,000 planes. Back in December the was “nearly 12 years” to clear, and just a few months later the backlog jumped to over 13 years.

Some airlines are responding by ordering many more planes than they need. Alaska Airlines just ordered 110 new Boeing narrowbodies and bought an option for 35 more, and when you read the language of the announcement carefully, a large part of the order was simply to hold more space in line, and “secure critical delivery slots” and thereby pay up front for some flexibility later. Their forecast is for 189 new aircraft to build new routes and replace older planes, but placed options for another 71.

So this all represents a big opportunity for COMAC, but also a serious challenge. The C919 is in active service in China, with high utilization rates in the markets where it is used. It’s now at 29 airports and flown by the three largest domestic carriers. But the challenge now is scaling up.

Next year COMAC hopes to produce 150 aircraft, and 200 per year starting in 2029. But that’s still not going to move the needle, much, on that global deficit right now of 17,000 planes.

Eventually we should expect that the commercial aviation industry will go the same way all the others have, and China will eventually take it over.

China has no problem buying titanium from Russia, for example. And there are no supply chain issues in China for aluminum, or in steel; no shortages of skilled labor. COMAC will sell all the planes they can build, and by 2050 will have blown up the duopoly that Airbus and Boeing have now.

But that’s a long way off, and things will be a lot worse for this industry until things are much better.

Be Good.

Resources and links:

China’s C919 jet poised to tackle ageing domestic fleet: industry official

https://www.scmp.com/economy/china-economy/article/3356365/chinas-c919-jet-poised-tackle-ageing-domestic-fleet-industry-official

The Countries With the Most Airline Passengers

https://www.statista.com/chart/34633/biggest-aviation-markets/

Airbus has warned of the risk of falling behind its delivery target. So far, it is ahead of Boeing

https://en.oninvest.com/article/airbus-has-warned-of-the-risk-of-falling-behind-its-delivery-target-so-far-it-is-ahead-of-boeing

Airbus’ Growing Inventory: Why the 2026 Delivery Target is at Risk Despite Growing Production

https://flightplan.forecastinternational.com/2026/04/30/airbus-growing-inventory-why-the-2026-delivery-target-is-at-risk-despite-growing-production/

Here’s The Real Reason Airlines Keep Ordering Aircraft They Don’t Need Yet

https://simpleflying.com/real-reason-airlines-keep-ordering-aircaft-dont-need-yet/

Reviving the Commercial Aircraft Supply Chain

https://www.iata.org/contentassets/85b59d951fc04c1c83fa2aab47824300/reviving-the-commercial-aircraft-supply-chain.pdf

Aerospace Supply Chain Bottlenecks Continue to Constrain Airlines

https://www.iata.org/en/pressroom/2025-releases/2025-12-09-02/

China’s C919 Jet Maker Get USD6.2 Billion Capital Injection From State-Owned Backers

https://www.yicaiglobal.com/news/comac-receives-usd62-billion-capital-injection-from-eight-state-owned-shareholders

Airbus Unsure of Reaching A320 Target Due to Pratt Problems

https://www.bloomberg.com/news/articles/2026-06-09/airbus-unsure-of-reaching-a320-target-because-of-pratt-problems

Airline Profitability Stabilizes with 3.9% Net Margin Expected in 2026

https://www.iata.org/en/pressroom/2025-releases/2025-12-09-01/

IATA, Jet Fuel Price Monitor

https://www.iata.org/en/publications/economics/fuel-monitor/

Alaska Airlines announces largest fleet order in airline’s history

https://www.sec.gov/Archives/edgar/data/766421/000076642126000004/ex991172026pressrelease.htm

Boeing captures 33% of single-aisle sector, maintains big lead for wide-bodies

https://leehamnews.com/2026/01/02/boeing-captures-33-of-single-aisle-sector-maintains-big-lead-for-wide-bodies/

COMAC C919

https://english.comac.cc/products/ca/

China’s COMAC will be bigger than Boeing and Airbus, combined, by 2040.

Inside China / Business is a reader-supported publication. To receive new posts and support my work, consider becoming a free or paid subscriber.

From Inside China / Business via This RSS Feed.