Bullets:

SpaceX will soon go public, in an offering that will value the company at over a trillion dollars.

Anthropic and OpenAI are Artificial Intelligence companies, who also plan IPO’s for later in the year.

Recent changes to indexing rules will compel massive share buys into these companies by retirement and pension plans, and by passive ETF’s and mutual funds.

In the past, new companies were required to wait until insiders sold most of the shares after the lockup periods before being added to investment indices. Companies also needed to show a strong history of growth and sound financial practices.

Inside China / Business is a reader-supported publication. To receive new posts and support my work, consider becoming a free or paid subscriber.

Report:

Good morning.

The heads-up on this story comes from one of our favorite Substacks, Gold and Geopolitics. Our concern is that the public, normal people, are at least unaware, and maybe even indifferent, to how really screwed they are at the highest level, and by people at the highest level. It’s not the kind of story that is felt tangibly, at least not at first, like a big spike in gas or food prices. And it’s also difficult to follow, and that’s exactly what the architects of our financial and political system are counting on.

It involves the qualification requirements for a new company to be included in the NASDAQ-100. The regulators changed those rules, so that new public companies can be part of the index. In the past, companies had to wait, and have a track record of revenues and profits. Because trillions of dollars’ worth of pension investments—which is money invested on behalf of workers, millions of private retirement plans, plus exchange-traded funds and other mutual funds, are invested in those indices. And they do so, assuming that the top 100 tech companies, in this case, are well-managed and profitable businesses.

But that rule is gone. Now, a newly public company can qualify, simply based on size—how big it is. And they changed the definition of “public”. Companies can qualify as a megacap public company simply by being large at the time of its IPO, then limiting how many shares they sell to the public. The index now accepts a weighting multiplier. That is what “small float” means—insiders of the company still own almost all of shares, and so completely control the company, even though it’s “public”.

They also threw out the rule for four consecutive quarters—one full year—of profits.

With these rule changes, the guardrails are down and regular Americans will be forced to buy shares of bad companies, that don’t make money.

The NASDAQ, in this case, gets big fees from the Initial Public Offerings of companies that want to avoid the rules that used to govern the industry, and protect small investors, somewhat, and SpaceX, in this case, will have tens of millions of passive investors buying their shares. That massive, passive buying will put a floor under the stock price no matter what happens, at the same time that insiders are allowed to dump their stock. Insiders and early investors are restricted from selling their shares during the IPO; they must wait to do so, until later.

That was previously a major risk to company insiders, and early investors: if the IPO price is set too high, or if the company does poorly after the IPO, their shares will be worth far less than they had hoped, just as they and all the other insiders are selling. But with these rule changes, passive investors will be buying shares, every single month, because they’re buying the index.

This is the source document. Paragraph 2 explains the new “fast entry” rules for new companies that list on the NASDAQ exchange. If the company’s market cap is in the top 40 of companies already there, it’s a Fast Entry addition, and will be put into the index after 15 trading days. So 15 days after the IPO, SpaceX will go into the index. The company will be exempt from “seasoning and liquidity requirements”—seasoning is how much experience the company has, earning money, and liquidity is how much money it has in the bank. Exempt.

Paragraph 3. These changes will go through, “without regard to free float considerations”. They changed the definition of “public company” and replaced it with a formula. So a public company is now one where just a tiny handful of shares actually are made available for sale to the public. A low-float company will just multiply the percentage of shares by five to meet the 10% float requirement, which goes away anyway for the new megacap companies.

SpaceX insisted on these specific rule changes in order for NASDAQ to get the listing, instead of the New York Stock Exchange. SpaceX wants early inclusion on the Nasdaq 100, which is the gold standard for large institutional investors, like pension and retirement plan managers investing in tech companies.

And there again—for executives and early investors, like private equity funds and venture capital firms—inclusion in the index now protects them from downward price moves. SpaceX goes into the index after 15 trading days, whereas insiders are required to wait 90 to 180 days to sell during their lockup period.

This is all every bit as bad as it sounds, and the head of the New York Stock Exchange is being as diplomatic as possible, considering that these rule changes mean that every giant new company will list on the NASDAQ from now on. New York has no chance now to get Anthropic or OpenAI, which are the next big IPO’s on the way. She says the Fast Entry rules—expedited index inclusion—artificially inflates valuations. And that’s the point. That’s just what insiders want, and just what the public should not want.

Substack writers are less cordial. Gold and Geopolitics calls it Graft, the active extraction of capital from passive, long-term investors to guys who just rewrote the rule book.

This one says the index is being rigged to appease a billionaire, who will be a trillionaire soon enough. It’s now a template for the forcible “transfer of wealth from the retirement accounts” of everyday Americans directly into the pockets of billionaire founders and billionaire VC funds.

George Noble is another Stack we like: “a shameless structural manipulation.”

The NASDAQ blew up the prestige of their own index just to get a stock listing. Every other public company up to now was required to meet minimum standards, at the very highest level, to qualify even for a public offering in the first place, let alone a designation as a top 100. All gone.

He explains the math here about what the 5x float multiplier means, and for companies qualifying for the index. But what makes that part much worse is that the small number of shares available to the public means that every single passive tech fund is chasing a small number of shares. The stock price is almost guaranteed to go up, starting on the 15th day, and insiders still get to own the other 95% of the company’s stock. The insiders who do sell have a guaranteed buyer: you. Your 401k plan, your pension.

The richest and most powerful people in the world can take a company public and never worry about the stock price, or ever losing control of the company. At least ten top officials in the Trump Administration stand to make millions on the SpaceX IPO. And let’s remember too that those same government officials can guide federal contracts to SpaceX already. Steve Witkoff isn’t in the administration, officially, but also has large holdings in SpaceX.

The new rules mean that fundamentals don’t matter. Valuations don’t even matter. Investment advisories do deep research into companies and prepare reports and estimates that are used by their clients and subscribers. Morningstar crunched the numbers on SpaceX and concludes that SpaceX is worth less than half what the IPO target raise is. The “company has been significantly overvalued”.

SpaceX will offer only 3% of the company’s shares to the public, which implies a more than $1.5 trillion valuation given the previous funding rounds.

Morningstar figures the company is worth $780 billion. This is a very good business; that is a huge number. Starlink is great technology, and SpaceX has an 80% market share in space launches. The other businesses—X, Twitter, and their AI investments don’t add up to very much, and even after modeling possibilities with Grok and Twitter, there’s no scenario that gets the company to $1.5 trillion.

But it doesn’t matter. The rules were changed, and not even Bloomberg can quite understand what it means, yet. But it doesn’t sound good. The SpaceX IPO is just the first of a bunch more megacap offerings and the integrity of the whole market is threatened:

Passive fund custodians are already modeling how to invest their trillions of dollars under management, because they have to. Their prospectus requires them to buy the index, no matter what companies are in, or how they got there. New exchange-traded funds and derivatives are also being created. The entire SpaceX float is just $75 billion, so all these funds have to fight over those shares which are a tiny—relatively tiny—share of the $1.8 trillion, or whatever the final number is. That’s to say that they have to weight their buys of the 3% of shares that are available, as if all the shares of the company were available to the public, which isn’t true.

This is Bloomberg, and they don’t know the rules anymore, or how anyone can follow them. But the balance of power on Wall Street is now unambiguously on the side of billionaire founders and private equity insiders; the institutions that at least claim to protect public investors aren’t even bothering to even pretend anymore:

The SpaceX IPO is coming in a few days. Next up is OpenAI and Anthropic, and they’re going to enjoy the same treatment. SpaceX would have been a blockbuster IPO, anyway. It is a good business; they have revenues and real products, but that is not something that’s true of AI companies. There are a handful of money managers who have come forward to say that SpaceX is uninvestable, fundamentally. They have ethical concerns too.

But none of that matters. Valuation doesn’t matter. Passive demand is what matters, and that will be almost unlimited, given the tiny number of shares they can buy, and the rules that say they must buy.

The NASDAQ 100 itself is $1.4 trillion in notional market value, including mutual funds at 75 billion, ETF’s like QQQ making up $587 billion more. Derivatives are 650 billion. All these market players are required to shift assets to SpaceX, whether Twitter or Grok makes money or not. Nothing matters.

And it’s all just in time for the new IPO’s for AI. We’ve covered the Artificial Intelligence industry a good bit on our channel, and the severe problems that Chinese AI companies pose the American hyperscalers, and AI companies like Anthropic and OpenAI.

Anthropic has filed for their IPO, and it would already qualify for inclusion into the NASDAQ 100 and the S&P, which means that their insiders will get the same guarantees that SpaceX just got. Hundreds of Anthropic employees will become millionaires, with huge paydays on the way for the seed companies, and none of them need to worry about the stock price going down before their lockout period ends.

And once again, doesn’t matter if the company makes money or not. Annualized non-GAAP revenue for the most recent month, times 12, gets a number is $47 billion. Not earnings—revenues. So the company IPO is 25 times annualized sales, or so.

Michael Burry is world famous for taking apart companies and systems and finding there’s nothing really there. SpaceX and Anthropic aren’t in the same league as collateralized mortgage obligations during the housing bubble, where loans to people who could not and would not ever pay them back were bundled together and sold off to institutional investors.

But he says there’s no way these companies are worth what the Wall Street underwriters claim, but the rules were just changed and it doesn’t matter anymore. The institutionals are the suckers again, and have to buy the shares anyway. Anthropic’s models cost too much, and costs are going up, while its users are leaving and services revenues are going down, and Anthropic insiders are rushing to cash out.

The SpaceX IPO and the rules changes will make Elon Musk a trillionaire, on paper, thanks to all the passive investors who will buy Space X in their ETF’s and retirement accounts. But the economics of AI companies posing a different set of problems for insiders, and for investors.

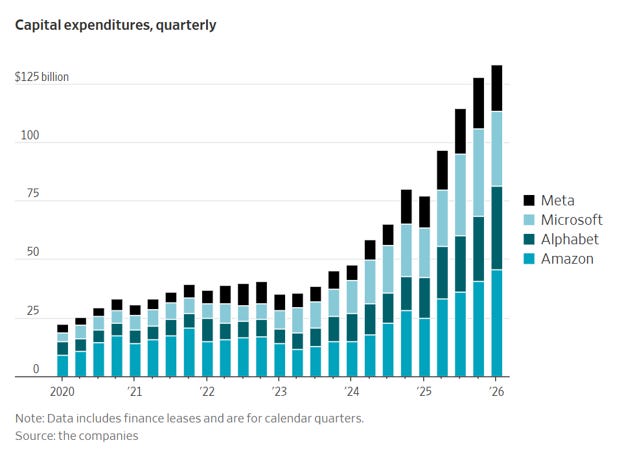

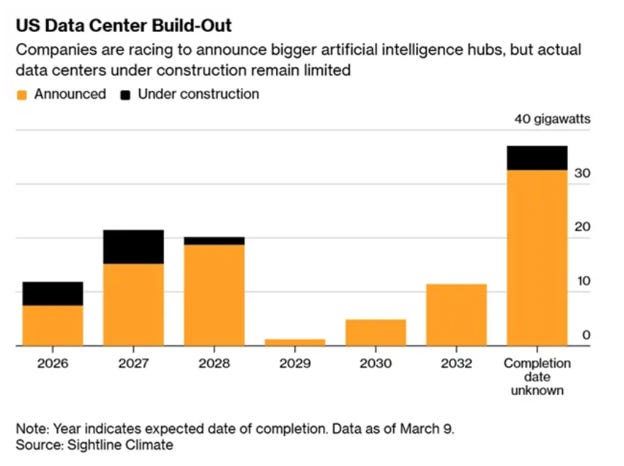

SpaceX has a wide moat in rocket launches, for example. Chinese companies launch rockets too, but the US government isn’t going to ask China for help putting up weather or spy satellites. But China is coming for AI, and the AI industry in the US has a lot of problems that are home-grown. Data center construction is slowing down, due to serious bottlenecks in the equipment to plug into the electric grids, which are under strain already. There is strong local opposition to new centers, almost everywhere. And without new data centers, the training of the large language models hits a hard ceiling:

All this CAPEX spend by the hyperscalers is contingent on data centers coming online, and they’re not. Half of projects that were supposed to be finished this year, aren’t even close, and looking out a few years, the construction of new centers has hit a wall:

Companies like Morningstar and Dow Jones used to matter, and if they said that a company was going public at more than twice what they thought it was worth, it would cause problems for underwriters. But those days are gone, and even Bloomberg knows none of this is good.

And we’re left to wonder just what, exactly, the Securities and Exchange Commission is supposed to be doing. And why it is that the only ones who have been screaming about these problems are in independent media, like Substack. The SEC is supposed to protect investors. Financial media is supposed to tell us what’s going on in industry, and in the most important companies.

But nobody is minding the store, anywhere. Ed Zitron is one the very best writers in the AI space, and is one of the Stacks we pay for. He is curious here, for example, what OpenAI’s numbers really are. OpenAI is ChatGPT, and generated $5.7 billion in revenue in Q1 of this year. Remember this is a company that underwriters think is worth over a trillion dollars. But the company has negative margins of 122%. ChatGPT is starting to charge users money for the service, and user growth suddenly stopped. It just costs a lot more to run AI programs than these companies are getting paid.

What’s worse, “large line items” were excluded. Stock-based compensation wasn’t counted, and if they had to report under GAAP rules, the losses could be a lot higher. But who knows? The company aims to make $30 billion in revenue, but earnings don’t matter anymore anyway. Fifteen days after the IPO, OpenAI is index-worthy and billions of dollars will pour in from investors.

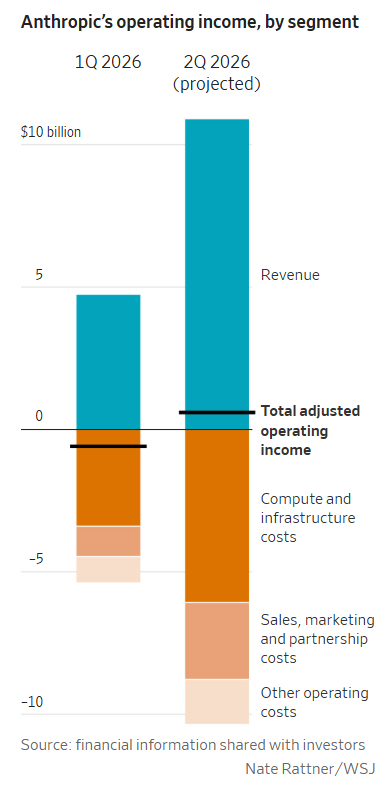

More funny math over at Anthropic. This is the headline from the Wall Street Journal. “Mind Blowing Growth” will propel Anthropic to its first profitable quarter. The startup expects a 130% revenue surge, its first operating profit, defying skeptics. Sounds amazing.

And here’s an amazing chart, with a black bar there, “adjusted operating income”, finally drifting over zero for the first time, in quarter 2. Which we are still in, by the way. But this is a forecast. What made that possible was a reduction in its costs for computing power, going from 71% of sales to 56%.

It’s unclear what accounting methods the company used, or what is the legal basis of some of the revenue. Don’t know if this is “mind blowing” but it does sound promising.

Not to Ed Zitron, though, who got busy and found it convenient that they figured out how to cut operating costs at just the exact same time they were looking for new funding, and learned from SpaceX’s S-1 that it’s a very temporary cost reduction, which can be canceled:

$15 billion a year in compute costs were discounted for two months in Q2—and only in the second quarter.

This is work the Wall Street Journal is supposed to be doing. That’s what the Securities and Exchange Commission is supposed to be asking questions about. Instead it’s left to “Where’s your Ed at?” and a handful of podcasts who are showing the world that the investment thesis for the entire American AI industry is blowing up. Costs are rising, not falling. AI data centers today are budgeted to cost $50 billion per gigawatt to build—and they’re not getting built anyway. Soon they’ll cost $80 to $100 billion per.

And the costs are rising just as companies who use the AI are realizing they’re not getting their money’s worth. Uber is a client of Anthropic, and has already spent its entire 2026 budget. Will they load up on some more tokens, to get through the rest of the year? Doubt it—it was a “head exploding moment” to learn how much Uber spent on tokens, which did NOT result in useful consumer features.

Alibaba is a Chinese company, and their Qwen large language model is the world’s most popular AI tool for business owners outside the United States. Airbnb tried to use ChatGPT to design a new reservation feature on their app, and even though the CEO of Airbnb is good friends with Sam Altman at OpenAI, his company switched over to Qwen instead. It works faster and costs less.

And that is catching on. Other companies are quietly making the switch to Chinese large-language models because they cost far less, and they’re open source and easier for their teams to use in their companies. The performance of Chinese models is similar to Silicon Valley’s best products, and are easier to use, cost less, and are more efficient. Companies are enterprise users—they pay for tokens, and executives lose their jobs if other executives heads blow up when they see their AI bill and ask what they’re getting for it. Companies are looking for alternatives to OpenAI and Anthropic, and signing up for DeepSeek instead. That also means that data is not going through US data centers, it’s coming to China instead, where electricity also happens to cost a lot less.

That could be the biggest challenge of all. For active investors – not the passive ones — business models matter. Revenues and profits – they matter. And the cost of compute is what is driving these corporate users of AI. They pay for the AI. Their engineering teams use it, every day, to develop new tools and applications, and they’re switching over to Chinese LLM’s.

Anthropic and OpenAI are fundamentally bad companies, with bad valuations, and produce financial reports that not even their own top executives trust. Their customers are moving away. And that used to mean that the insiders cannot cash out and make billions of dollars. They might even go to jail. But that was before they changed the rules, and so they’ll make you buy them instead.

Be Good.

Resources and links:

Gold and Geopolitics, Honest graft

[ Gold and Geopolitics

Gold and Geopolitics

Honest graft

As a thanks to my paid subscribers they received this article yesterday. After a day, it opens up for everybody else…

Read more

6 days ago · 111 likes · 33 comments · No1](https://no01.substack.com/p/honest-graft)

NYSE President Criticizes Nasdaq’s Rule Changes Amid SpaceX IPO

https://phemex.com/news/article/nyse-president-criticizes-nasdaqs-rule-changes-amid-spacex-ipo-84650

How to rig an index to appease a billionaire

[ Keubiko’s Musings

Keubiko’s Musings

Nasdaq’s Shame

Disclaimer: The following article is for informational purposes only and represents the opinion of the author. It should not be construed as investment or any other kind of advice. All information is based on publicly available data believed to be accurate as of the date of publication, but the author makes no representations or warranties as to its com…

Read more

3 months ago · 524 likes · 48 comments · Keubiko](https://keubiko.substack.com/p/nasdaqs-shame)

Reuters, SpaceX weighs NASDAQ listing after seeking early index entry

George Noble, The Noble Update

Trump Officials Held Millions of Dollars of SpaceX Ahead of IPO

SpaceX: What Investors Need to Know About Its Enormous Upcoming IPO

https://www.morningstar.com/stocks/spacex-what-investors-need-know-about-its-enormous-upcoming-ipo

Morningstar values SpaceX at $780 billion, half its IPO target

SpaceX is worth less than half of its $1.75 trillion IPO target, Morningstar says

https://www.cnbc.com/2026/06/03/morningstar-spacex-ipo-target-price-nasdaq.html

SpaceX’s IPO Forces Wall Street to Reorganize Around It

America’s Data-Center Build-Out Is Falling Way Behind Schedule

https://www.wsj.com/tech/ai/americas-data-center-build-out-is-falling-way-behind-schedule-e408a9a8

‘Big Short’ investor Michael Burry says neither SpaceX nor Anthropic is worth $1 trillion

https://www.businessinsider.com/big-short-michael-burry-spacex-anthropic-ipo-ai-bubble-claude-2026-6

The U.S. and China Lead The Space Race 2.0

https://www.statista.com/chart/28667/countries-are-leading-the-space-race-20

OpenAI’s OWN CFO just admitted they cannot pay their bills.

Alibaba’s Qwen family captures over 50% of global open-source downloads, report finds

$64 billion of data center projects have been blocked or delayed amid local opposition

https://www.datacenterwatch.org/report

Investor alert: Chinese AI is booming in global markets, and Huawei’s chips beat Nvidia’s

The AI industry in the US is doomed. Now China owns it all.

Initial Public Offerings: Lockup Agreements

Uber’s COO says it’s getting harder to justify the money spent on AI tokenmaxxing

https://www.wheresyoured.at/author/edward/

Amazon and Google have billions riding on Anthropic. The IPO will finally reveal how much.

https://fortune.com/2026/06/04/amazon-google-billions-anthropic-ipo/

TechCrunch, Ahead of its IPO, Anthropic’s Amodei shrugs off doubts about AI returns

Nasdaq-100 Index® Consultation – February 2026

https://indexes.nasdaqomx.com/docs/NDX_Consultation-February_2026.pdf

Exclusive: Elon Musk’s SpaceX weighs Nasdaq listing after seeking early index entry, sources say

Danish Pension Blacklists SpaceX Over ‘Catastrophic Governance’

Mind-Blowing Growth Is About to Propel Anthropic Into Its First Profitable Quarter

Where’s Your Ed At?

https://www.wheresyoured.at/author/edward/

https://www.wheresyoured.at/where-are-all-the-data-centers/

Why Airbnb switched from OpenAI to Chinese AI (and what it means for your budget)

Airbnb ‘relies heavily’ on Alibaba’s Qwen models to power its AI customer service agent, CEO Brian Chesky says

Cheap and Open Source, Chinese AI Models Are Taking Off

https://www.thewirechina.com/2025/11/09/cheap-and-open-source-chinese-ai-models-are-taking-off/

More US firms turn to China’s DeepSeek over pricey Silicon Valley AI

Inside China / Business is a reader-supported publication. To receive new posts and support my work, consider becoming a free or paid subscriber.

From Inside China / Business via This RSS Feed.