Bullets:

China dominates the global chemicals industry, and leads the world in chemistry and research.

A major driver is China’s boom in manufacturing, which requires robust supply chains for chemical inputs, and top chemistry engineering talent.

Chinese monopolies in cutting-edge chemical research, and massive production capacities which slash manufacturing costs, mean that China’s policymakers can restrict its exports and final use, for example to weapons makers.

Top European chemical companies are cutting production lines and jobs in home markets, to build production and create jobs in Mainland China.

Inside China / Business is a reader-supported publication. To receive new posts and support my work, consider becoming a free or paid subscriber.

Report:

Good morning.

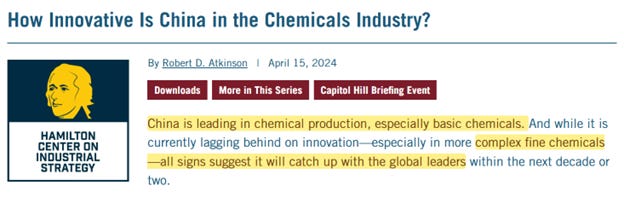

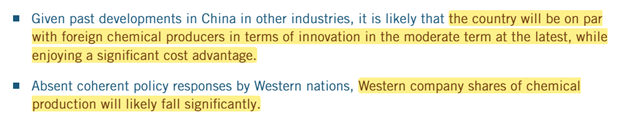

This is a report from almost exactly two years ago. It’s from the Information Technology and Innovation Foundation, and is a deep dive into the Chinese chemical industry. They concluded at that time that China was already leading in the production of chemicals, and was catching up quickly with industry leaders in other countries for more complex chemicals.

By 2022, China already was 44% of global production of chemicals, and 46% of new capital formation and R&D spending. Here are some of their predictions, from 2024: Chinese policymakers are determined that the chemical industry will be self-sufficient, and it is “likely that the country will be” comparable to foreign chemical companies with respect to innovation in just a few years, at the latest. China already enjoyed strong cost advantages, which meant that Western companies’ global manufacturing share would probably fall—significantly.

This is a $5 trillion industry, and comprises four large sectors: basic chemicals, ag, and the consumer segments. Chinese companies invest much more in R&D compared to peer countries and companies outside China, while also enjoying strong industry support from government.

The conventional wisdom in the chemistry field was the same as in everything else: cars, planes, semiconductors—that China is a copier, or at the most a “fast-follower”, while North America and Western Europe are the innovators.

The United States believes that they can attract top talent from across the world, and something magic happens when they show up, and they can create and innovate faster than if they had stayed home. There are lots of problems with that idea, as we see in just about every single industry there is. China’s costs are lower, so companies in China can afford to experiment with new technologies.

And it was always a weak thesis, anyway, that Chinese researchers are waiting around for American or German or Japanese scientists to do the work, then get busy working on knockoffs. It just doesn’t survive scrutiny.

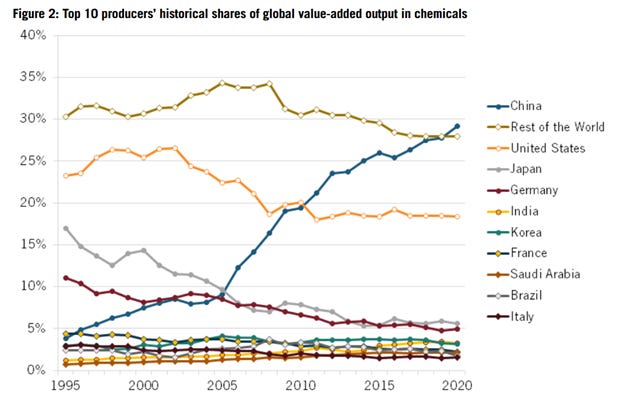

These data are already six years old, from 2020: China was already the single highest source of value-added output in chemicals. That is not basic chemicals mass-production, then—this is surplus value created, and by 2020 was over 50% higher than the chemical industry in the United States.

There is only one market where that metric is moving sharply higher, over time. China’s value-add in 1995 was less than half compared to Saudi Arabia. India, in 2005, generated more than twice the surplus value of China. By 2010, China passed India. By 2023, China’s share of global market sales was over 40%, and China saw the highest capital investment intensity, 2.8 times more than the United States.

A primary driver of all of that, is that this is where the demand is, for chemicals of all kinds. And that’s another metric that has gone vertical—as Chinese manufacturing boomed, they needed a chemicals industry to feed their factory sectors, and that need continues to grow.

By 2024, Chinese chemical companies were already snapping up market share from competitors. This is a slow-growth, low-margin industry. There is a relatively small number of commercially viable products that are developed each year. It’s a mature industry, and investors need to be patient, and that’s a big part of the problem. Chinese companies have a lower cost of capital, lower borrowing costs, and lower operational costs structures. Western firms operating in North America and Europe don’t enjoy any of those advantages, and what’s more they answer to Wall Street investors who want to book short-term profits at high hurdle rates.

This is all to say that Chinese companies can afford to expand, today, in expectation of future demand, while Western companies cannot do so in their home markets. China is where the market is, and foreign companies have no choice but to invest heavily here, just to stay competitive in the Chinese market, selling chemical products to Chinese industrial users.

By 2022, 34% of Research and Development in the chemical industry was invested here, in China. And by the way, R&D dollars go a lot farther in China, compared to the United States or in Germany. And that boom in R&D has translated into new patents by Chinese firms and research institutes.

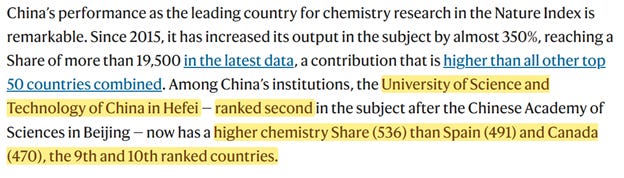

Now it’s 2026, just two years after that report from ITIF. China is now inarguably the leading country for chemistry research. In the past 10 years, China increased its research by four and a half times. Now China’s share of top research is higher than the next 50 countries combined. The University of Science and Technology is China’s second-ranked university for chemistry, and that single institution has a higher share than Spain and Canada—entire countries.

That focus on chemistry means that China, and Asia generally, now decides which chemicals get built and how they’re used, and obviously where they’re used. We mean here that China can use their emerging monopolies in chemical manufacturing, and deny them to weapons makers, for example—just as they have already done in rare earth metals, magnets, and industrial diamonds.

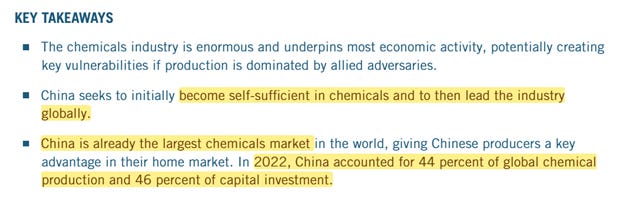

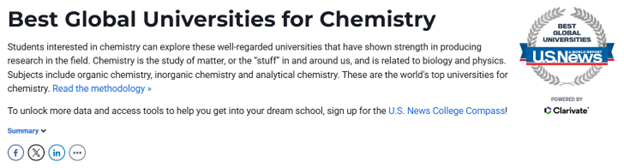

Here are the global university rankings in chemistry. USTC is at #2. Tsinghua in Beijing, and is top in the world. Unis in Singapore show up at #3 and #4; Stanford is ranked #5. Then it’s a lot of Chinese flags there in the top 30.

What does that mean for students, for young people across the world, who want to study chemistry, then actually get a job after? Where are those jobs in chemistry going to be?

We already know the answer to that, and so do the biggest chemical companies across the world. That is the CEO of Clariant, which is a giant Swiss chemical company. The Chinese market is bigger than the United States and Europe put together, so Clariant was already moving their money. In 2020, 10% of Clariant’s sales came from China—402 million Swiss francs. So Clariant opened a 45 million Swiss-franc R&D center in Zhejiang. In 2023, Clariant shut down facilities and cut jobs in Europe—the company closed a plant in Romania and downsized operations in Germany. They had invested in a plant with a capacity of 50,000 tons a year but never produced that much. Their Podari facility lost 77 million Swiss Francs.

Clariant turned around and invested that same amount—80 million CHF-- in a new facility in China, at Daya Bay which, by the way, is home to some of the biggest nuclear reactors in China. So we should assume that by parking their new plant right next door, Clariant doesn’t have to worry anymore about affordable electricity. Energy costs in the EU blew up along with the Nordstream, and Russia shipping their crude and natural gas to China instead of Western Europe, and that has made European manufacturing impossibly uncompetitive and unaffordable.

BASF is the biggest chemical company in the world, and they’re doing the same—closing production in Europe to open new capacity here in China. BASF is headquartered in Germany, where the company is laying off thousands of people to invest here, along with leading automakers and equipment manufacturers. “Surging energy costs”—that’s often the first reason cited by business executives getting ready to move their production. It’s true, but also relatable to the people about to lose their jobs. Europeans generally see it in their own utility bills. They’re aware that it costs a lot more to keep the lights on at home than just a few years ago, while they are likely unaware that in the roster of top universities to study chemistry, European unis don’t hit the list until ETH Zurich, at #25, and Germany doesn’t show up at all. The costs are too high to be competitive with Asia right now, and the talent pipelines for the future have also already moved away.

Europe has seen an erosion of manufacturing industry generally, along with business confidence and investment, which is a cycle that feeds on itself. China, meanwhile, is going the other way. BASF is shutting down facilities in Germany, laying off thousands of people there, and investing in cutting-edge plants in China, hiring thousands of people here.

We do appreciate these analyses, and wonder why we cannot find more of them. It isn’t particularly difficult to see charts like those, confirm that the data are right, and then ask, what does it mean if those trends continue, for just a little longer?

And then to ask, what might happen to accelerate them—and make them worse–for example an energy supply chain shock, like Russia-Ukraine in 2022, or another war in the Middle East, but this time against someone who can close the Hormuz?

The trends did continue in China, and did get worse in Europe, and today the biggest chemical companies in the world have decided that the chemical industry in Europe is gone. It has no future, because manufacturing industry in Europe has no future. So those companies are moving.

And that is all good for young people to know. If you want to study chemistry, or work in chemistry, you can’t stay in Europe either.

Be Good.

Resources and links:

Charted: China’s Rise to Manufacturing Dominance Over 30 Years https://www.visualcapitalist.com/china-vs-americas-industrial-growth-2019-2024/

Best Global Universities for Chemistry

https://www.usnews.com/education/best-global-universities/chemistry

What China’s rise in chemistry means for the rest of the world

https://www.nature.com/articles/d41586-026-00428-9

BASF launches biggest overseas project in China with green-powered mega-site

https://www.scmp.com/business/article/3348021/basf-launches-biggest-overseas-project-china-green-powered-mega-site

Clariant CEO: China chemicals market bigger than U.S. and Europe combined

https://www.cnbc.com/video/2025/11/20/clariant-ceo-china-chemicals-market-bigger-than-u-s-and-europe-combined.html

Chemical market overcapacity and weakening demand: a perfect storm

https://www.icis.com/explore/resources/chemical-market-overcapacity/

How Innovative Is China in the Chemicals Industry?

https://itif.org/publications/2024/04/15/how-innovative-is-china-in-the-chemicals-industry/

BASF Agricultural Solutions plans to change production network of glufosinate-ammonium

https://www.basf.com/global/en/media/news-releases/2024/07/p-24-230

German ‘chemical town’ fears impact of industrial decline

https://www.france24.com/en/live-news/20260517-german-chemical-town-fears-impact-of-industrial-decline

BASF drives forward structural adjustments at the Ludwigshafen site and closes production plants for adipic acid, CDon and CPon

https://www.basf.com/global/en/media/news-releases/2024/08/p-24-269

BASF quietly closed 11 factories in Germany and transferred to China for plant investment

https://www.echemi.com/cms/1939901.html

BASF: 2024 at a Glance

https://report.basf.com/2024/en/overviews/2024-at-a-glance.html

Clariant to cut 170 jobs after closing Romania plant, downsize German operations

https://www.reuters.com/business/clariant-cut-170-jobs-after-closing-romania-plant-downsize-german-operations-2023-12-06/

Inside China / Business is a reader-supported publication. To receive new posts and support my work, consider becoming a free or paid subscriber.

From Inside China / Business via This RSS Feed.