Bullets:

Savvy trading companies are making billions in risk-free profits, as dislocations in oil markets ripple across the world.

Real-world buyers of oil are paying high premiums bring in new supply, while futures traders have wagered–wrongly so far–that prices would soon fall as supply resumes.

The shortages were first felt in East Asia, in major refining hubs in Singapore, Japan, Korea, and India. Spot prices rocketed immediately following the closure of the Strait of Hormuz.

But prices were suppressed in North America, and particularly on NYMEX futures markets for WTI.

We explain the mechanics of an arbitrage trade, and how commodities traders earn billions in profits.

Inside China / Business is a reader-supported publication. To receive new posts and support my work, consider becoming a free or paid subscriber.

Report:

Good morning.

Previously we pointed out that there was a very large disconnect across different energy markets. First there was a big difference between what oil futures traders were doing, compared to what oil consumers were paying for oil in the real world, where ships need to move and planes need to fly.

For the first couple of weeks of the war on Iran, oil traded in US markets in particular seemed far out of line with the real-world price of oil was at the time. There was also a dislocation—the oil was in the wrong place. At the time, oil was in surplus in the United States and Canada, and ironically in China, but in severe shortage almost everywhere else.

That entire situation is ripe with opportunity, for companies and institutions who can operate on these trading exchanges, and who can physically move oil from well-supplied markets to the ones desperate for supply; to buyers who will pay big premiums to get it. This is a top analyst who writes for Bloomberg, who explains that the oil market is global, and how much a barrel of oil is worth depends very much on who is answering the question, and from where.

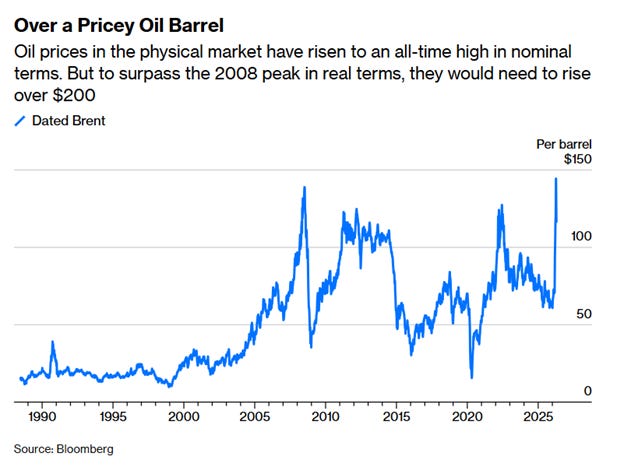

Immediately the price for Brent crude went vertical; Brent is the reference index for Europe. Meanwhile the WTI index, West Texas Intermediate, did not move nearly as fast or as high, until later:

There are two markets. The physical is the real-world market, and the paper market is speculators buying and selling oil contracts to be settled later. Physical reflects supply and demand today, and how easily barrels and ships can be moved around, and how fast.

The paper market is theoretically infinite in size when the contracts are created, then as the contracts get closer to expiration, they either expire because they’re out-of-the-money, or the paper prices converge to real-world physical supply and demand. For example, the physical market lost over 10 million barrels of real-world oil because of the closure of the Strait of Hormuz, but the paper market traded an extra million barrels. That surplus million barrels don’t exist in the real world, and so the contracts will expire with one side or the other losing their premiums.

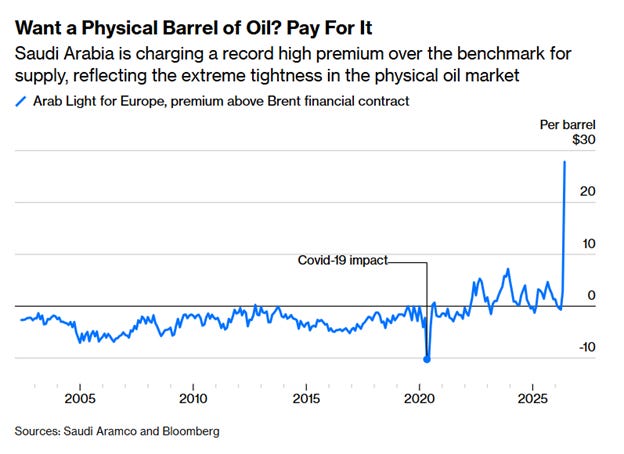

The physical world is different. Airlines, for example, either pay up for energy, or keep planes on the ground, or a combination of both. So the premiums paid for physical oil, today, blew out to record highs. Saudi Arabia is using a pipeline to move oil and ship from different ports, bypassing the Strait of Hormuz. But the volumes through the pipeline are far below what ships can carry.

Saudi took advantage, and was charging premiums of about $28 per barrel, compared to the paper contract. Just before the war Saudi Arabia was selling their oil at a discount, of 65 cents. Physical barrels just aren’t there.

Then comes the transportation problem. Logistics used to be taken for granted. Now the shipping costs for a barrel of oil are shooting higher. Transport costs pre-war were $1 a barrel. Now they’re $25:

Insurance is expensive, assuming buyers can get it at all. Those extra costs do not show up on paper oil trading screens because nobody has to buy it yet, but as soon as paper becomes physical, those costs become real. He points out here that these are two markets, generally functioning as they should: physical market is still telling us the price for the next 30 days, the paper market is trying to figure out the price after 60 days.

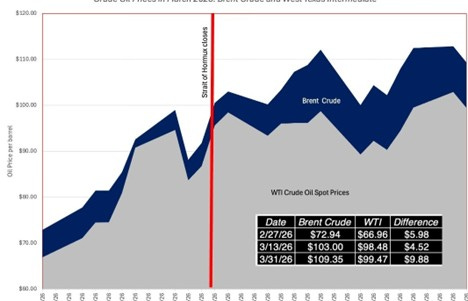

The dislocation, we can say, is getting fixed, and this is how. Oil shortages appeared right away in East Asian markets—like in Japan, Korea, Singapore. And right away refineries here in East Asia were paying whatever they had to, higher than $175 a barrel. Then those demand and price pressures moved to Europe.

After that it was just a matter of time before supertankers were headed to the United States. In the opening few weeks of the war, prices in the US did NOT move as much as – almost anywhere --else; now the ships are filling up and hauling the oil away, and shortages are hitting even in North American markets. For example, no Asian airlines yet have needed to shut down because of fuel prices, but Spirit Airlines is gone, and the clock is ticking on a handful of others there too.

This all represents a massive arbitrage opportunity. The prices on trading screens are completely divorced from the prices paid by real-world buyers and sellers to move energy around. Then we saw North American oil markets still in surplus—temporarily; briefly—while rich countries in Asia and elsewhere were in shortage.

It’s a bonanza for commodities traders, who operate in both the physical and paper markets, and have the logistics to move oil from one place to another. Vitol is a commodities trader, and lost a lot of money in the first days of the war when prices moved violently against them. They also have ships are stuck behind two blockades now, and cannot get through the Strait of Hormuz. Since then, Vitol has recovered all those losses, and have made profits of $2 billion.

Mercuria reports their return on equity is at the high end of its normal range, implying that their profits just so far are $2.3 billion. These companies are taking physical oil, moving them, and pocketing record-high premiums.

This is a beautiful example of how, in a nuts-and-bolts way, this kind of trade works. Again, this was widely understood, weeks ago, that the paper barrels in the United States were way out-of-line with what was happening in the real world, everywhere else. The question is, what can anyone do about it?

If you saw this chart oil of oil futures from 13 April, you would think that the market was pricing in a lot more supply coming online. The price dropped at the open, even though that was when the US Navy’s blockade of the Iranian Navy began. It made no sense.

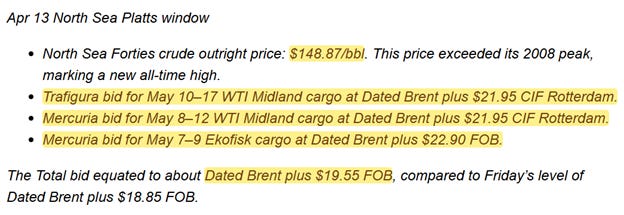

That is what the commodities traders also saw, and what they did. North Sea crude price—that’s physical—was $148.87 per barrel, and the training companies placed these bids on the US exchange, for West Texas Intermediate for delivery in May. The May WTI contract was trading at $96 per barrel. The June contract was trading at $90 a barrel. That is called “backwardation”, when lower prices are expected in the future. That $6 per barrel backwardation is also highly unusual, far higher than normal. And if prices continue to move higher—and they have been—a lot of traders for the June contract are in trouble. But for that day, the physical crude markets were $50 a barrel over the prices for May. That situation then is a “reverse cash-and-carry” arbitrage. The futures price is deeply discounted compared to physical, today.

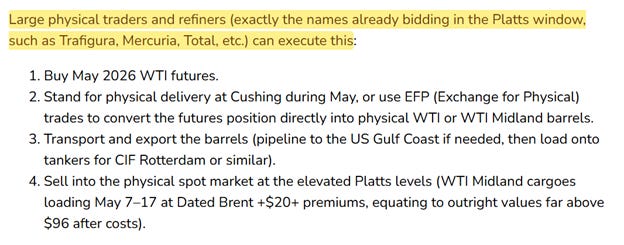

Here is the trade—buy the May 2026 futures contract, on the WTI:

In May, take physical delivery. Then transport the barrels from Cushing, Oklahoma to ports, and load them onto tankers heading to Europe. Then sell those barrels into the physical market. The net spread would be about $40, before logistics and financing of around $8-15 per barrel.

The other advantage for these companies, is that while the crude is on the ocean, heading to markets, they can still shop for and hit other bids, then send the ship in a different direction. These profits are locked in almost everywhere.

Everyone in the energy markets knew at the time, that even were the war to end today, it will take a long time for new oil barrels to get delivered to markets. Everyone in the Persian Gulf needs to turn their wells back on and everyone else needs to get ships turned around.

And so when politicians tell us that oil prices will “drop like a rock” as soon as the war is over—it’s true, in a way. On trading screens, and on oil contracts three months out, that is probably true. But in the physical world, it will take a lot longer.

Be Good.

Resources and links:

So What Is the Real Oil Price Right Now?

https://www.bloomberg.com/opinion/articles/2026-04-18/iran-war-what-is-the-real-oil-price-right-now

WHY WHO’S F/AROUND IN THE OIL FUTURES MARKET MIGHT FIND OUT IN 7 DAYS

https://justdario.com/2026/04/why-whos-f-around-in-the-oil-futures-market-might-find-out-in-7-days/

Commodity Traders Reap Billions in Profit as War Upends Markets

https://www.bloomberg.com/news/articles/2026-04-21/commodity-traders-reap-billions-in-profit-as-war-upends-markets

Vitol Made About $2 Billion in First Quarter Despite War Losses

https://www.bloomberg.com/news/articles/2026-04-19/vitol-made-about-2-billion-in-first-quarter-despite-war-losses

$140, and going higher: That’s the real price of oil, right now. Oil traders will be wiped out.

More Airline Bankruptcies May Be Coming — JetBlue And Frontier Face The Highest Risk

https://viewfromthewing.com/more-airline-bankruptcies-may-be-coming-jetblue-and-frontier-face-the-highest-risk/

Bloomberg, Fuel Tankers U-Turn to Asia as War Worsens Supply Crunch

https://www.bloomberg.com/news/articles/2026-03-09/fuel-cargoes-redirecting-to-asia-with-supply-crunch-worsening

Reuters, Trump says gas prices will drop as soon as Iran war is over

https://www.reuters.com/business/energy/trump-says-gas-prices-will-drop-soon-iran-war-is-over-2026-04-30/

Inside China / Business is a reader-supported publication. To receive new posts and support my work, consider becoming a free or paid subscriber.

From Inside China / Business via This RSS Feed.