Bullets:

China invested heavily over decades to develop their domestic mining industry.

But outbound investment soared since 2013, under the Belt and Road Initiative. China has thereby locked up critical raw materials supply chains in countries that are far more friendly with China, than with the United States.

Beijing has enacted export bans on the use of those metals, for use by weapons makers. For the Pentagon, the obvious answer is to build an end-to-end supply chain for rare earth metals and other minerals, to get around those export bans.

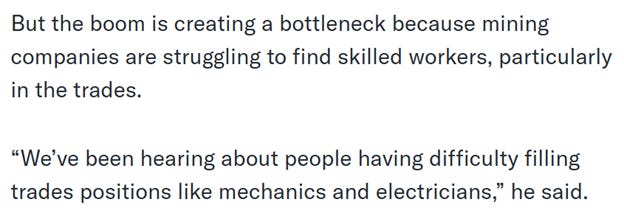

But the problem is a lack of engineers and mine workers. Across the United States and Canada, a severe shortage of skilled tradesmen preclude an expansion of the mining industry.

Inside China / Business is a reader-supported publication. To receive new posts and support my work, consider becoming a free or paid subscriber.

Report:

Good morning.

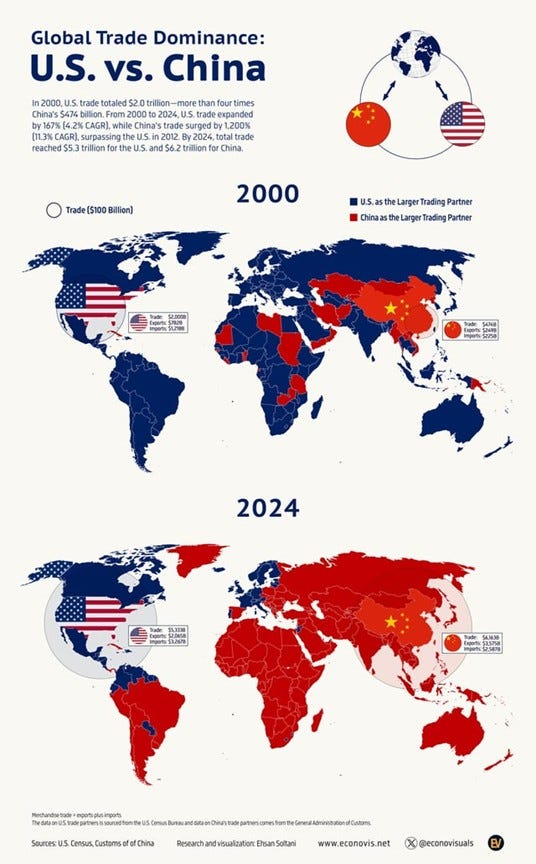

This map is a strong example of how the world has changed in just two decades. Country by country, who is the bigger trading partner, the United States, or China? In 2000, almost everyone did more trade with the United States, than with China. In the Western Hemisphere, Cuba was the lone exception. All of Europe, even Russia.

By 2024 it’s a different world. All of Africa. Australia and New Zealand. Most of South America. All of Eastern Europe, except for the Baltic states. So these trading relationships represent real investments, and real-world buying and selling, and China is a dominant trading partner for most of the countries on the world map today.

And Pentagon officials and weapons makers are confounded with the problem now, that China has global monopolies on the mining and refining of rare earth metals, which are crucial for modern manufacturing, and particularly for those big Pentagon contractors. China has export bans on rare earth metals that are used by defense contractors, and now there are shortages of all of them, outside China and the BRICS countries that are friendly with China.

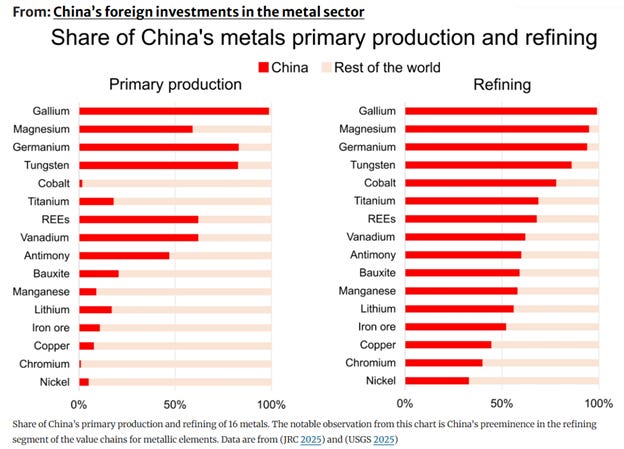

The reliance on China for this supply chain is almost total. The US Geological Survey published their list of 50 critical minerals, and the United States relies on imports for 31 of those fifty – with imports over 50% of demand. And for nine of them, China was the exclusive supplier.

The Pentagon is especially dependent on China, with 78% of military systems reliant on critical minerals from China. They got there after decades of investment and development of their mining industry, at home and across the world. They built universities and research centers that produce more patents in the industry than in the rest of the world combined. They also are dominant in the refining industries, of these metals. Across the US, Europe, and Japan there is just a handful of people who know how to do that work, whereas China has thousands of them.

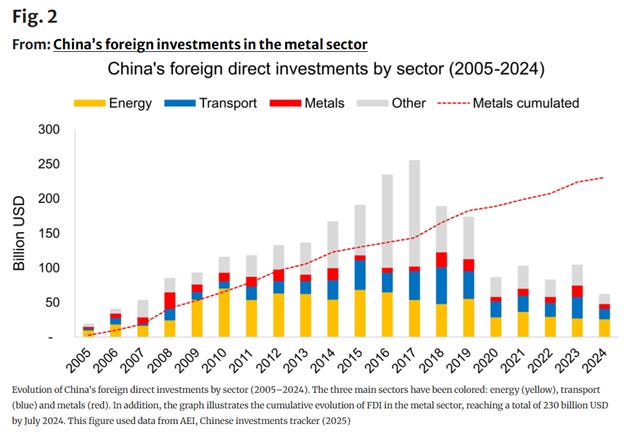

But we need to refer again to that trading map, and understand that this was the result of decades of deliberate national policy. China’s Belt and Road Initiative was launched in 2013. The purpose was to reinforce—make stronger—bilateral cooperation between China and 150 countries across the world, and to lock down raw materials supplies needed by China’s industrial sectors. In particular, the metals and minerals that are essential to electronics, power generation and distribution, and consumer and household products. The technologies of tomorrow, in other words, as well as what we need right now to sustain modern life. The Foreign Direct Investment was strongly encouraged by Chinese government authorities, which would develop a global value chain system, and strong relationships with partner countries. China’s industrial needs would be coupled with development strategies in partner countries.

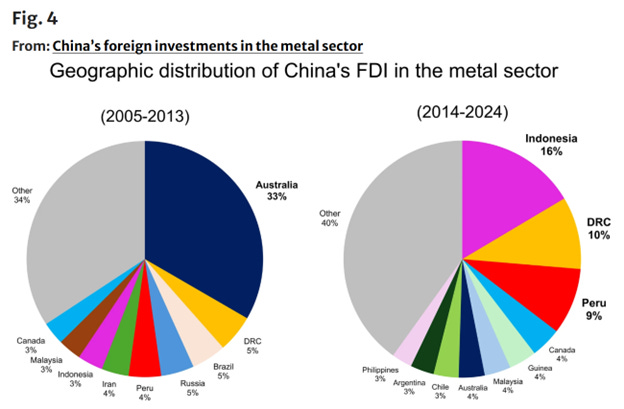

For the metals, cumulative Chinese FDI is on that dotted red line, and now stands at $250 billion. The Belt and Road Initiative not only expanded FDI, but also redirected the investment flows: before 2013, Australia claimed a third of Chinese outbound investment. Since 2014, it’s just 4% to Australia. Massive new investments from China into Indonesia, up over five times. Democratic Republic of Congo and Peru, more than doubled. Double-digit percentage increases in over a dozen countries, in absolute terms:

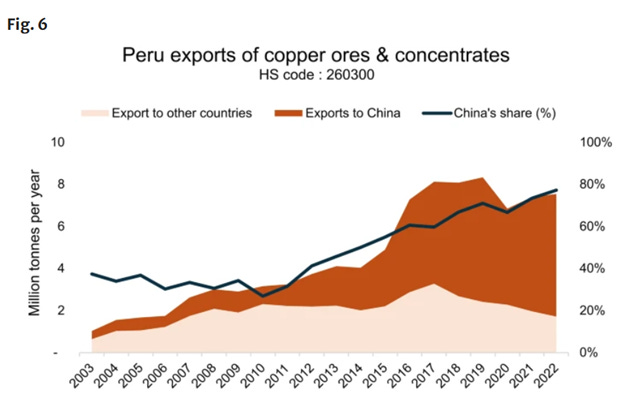

Taking one country, Peru, as an example of how this has played out, over time. In 2003, Peru’s exports of copper ores to China were under one million tons, which was 40% of Peru’s total. So China was a major buyer, and Peru’s copper ores industry grew rapidly until 2013. China Belt and Road was announced in 2013, along with huge increases in outbound FDI to Peru. Now China takes 80% of Peru’s global exports of copper, which today is six million tons:

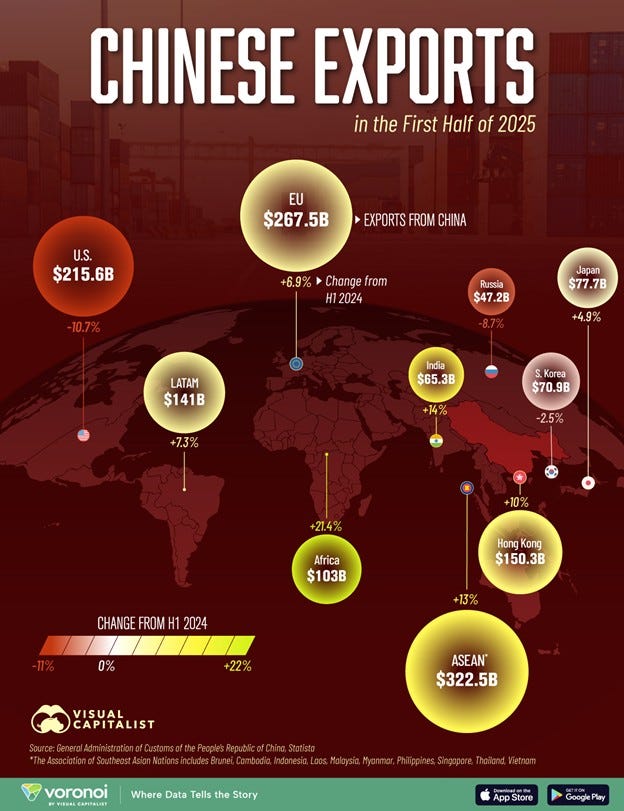

And the trade is two-way—raw materials are going out, manufactured products going back. 2025 was a trade war year between the United States and everybody, but China most of all, and Chinese exports to the US dropped by over 10%, to $215 billion in the first six months. But that was easily made up for, with export booms to ASEAN countries, up to over $300 billion. South America exports, up to $141 billion, Africa now over a hundred billion.

Countries in the Belt and Road program develop new metals and mining industries and exports to China boom, and feed the Chinese factory sectors. Then ships going the other way are modernizing and electrifying economies in the Global Majority countries at the fastest pace in history.

So again the Pentagon problem comes from the fact that the same minerals and metals they need to build bombs, are the same ones Africa and South America and Asia need for power stations and cars and refrigerators and smart phones, and mining companies across the world seem to be much happier doing that business with China. And let’s hit this point again, which is that civilian manufacturers in the United States are able to get these metals from China; the export bans only apply to companies that build things that blow up people, and it’s those companies that can’t get the raw materials they need.

The obvious solution is to build an end-to-end supply chain for these metals, in North America. We’ll focus this time on just the first part, the mining; getting the raw materials out of the ground, and in particular the people problem.

China is already far ahead. In the 1980’s, the United States had more than twice as many mining schools as today. Those schools now turn out around 300 mining engineers per year. In China, it’s over 3,000 per year. That ratio, by the way, holds firm across many other disciplines: 1.3 million Chinese graduates in engineering, every year, compared to 130,000 in the United States. That is a 10-to-1 ratio, and we pointed out previously that many of the engineering graduates from US universities are not US citizens in the first place, and after picking up their degree head back to where they came from.

So the pipeline of new engineers isn’t anywhere close to where it needs to be to make mining in the United States even viable, let alone competitive. Six hundred new mining engineers a year are needed, and American schools produce only half that. At the other end, workers are leaving. The workforce for the mining industry is old, and on the verge of retirement. More than half of the workforce will retire in the next four years.

It’s an industry-wide problem, and it’s the same story up in Canada. Besides a severe shortage of mining engineers, the industry doesn’t have enough of everybody else that mines need to run. Industrial electricians, mechanics, welders—they’re all at critically short levels too. For example, a Canadian company in the nuclear industry is short fifty welders.

This isn’t a money problem. These companies have plenty of money; what they lack is people. The unemployment rate for skilled tradesmen—and they’re almost all men—is basically zero. And for young people with those skills, there are other options besides hazardous work in extreme weather, usually far from home. Just six percent of mining workers in Canada are under the age of 25. And so well-funded mining projects can fall apart if anything goes wrong on the staffing side—there is just no slack in this system, industry-wide. In China and in the Global Majority countries, there is excess capacity. This scenario, described here, is unthinkable on a Chinese mining project, where one guy isn’t feeling well and the whole company shuts down until he’s better:

The thesis here, from this think tank, is that the only way out is through high levels of immigration. The thinking is that since the Pentagon isn’t allowed to import the rare earth metals and minerals their contractors need to build weapons systems, they will instead import the people who already know the mining business. Like Chinese, I guess. Or the guys in Peru.

So that’s the plan now.

Be Good.

Resources and links:

Building a domestic critical mineral workforce through immigration

https://www.niskanencenter.org/building-a-domestic-critical-mineral-workforce-through-immigration/

‘The hottest it’s ever been’: Skilled labour shortage is tapping the brakes on Canada’s mining boom

https://ca.finance.yahoo.com/news/hottest-ever-canada-mining-sector-150822574.html

Building a domestic critical mineral workforce through immigration

https://www.niskanencenter.org/building-a-domestic-critical-mineral-workforce-through-immigration/

US mining’s talent crisis

https://www.miningmagazine.com/americas/news-analysis/4528102/us-minings-talent-crisis

Urgently needed: more mining workers

https://www.theglobeandmail.com/business/adv/article-urgently-needed-more-mining-workers/

Mining.com, Mining growth creates trades worker gap in Ontario

https://www.mining.com/blog/mining-growth-creates-trades-worker-gap-in-ontario

China graduates 1.3 million engineers per year, versus just 130,000 in the U.S. We need AI to bridge the gap

https://fortune.com/2026/01/14/china-graduates-1-3-million-engineers-per-year-us-shortage-ai-tools/

U.S. Mining Push Faces Workforce Shortage

https://nationaltoday.com/us/tx/el-paso/news/2026/02/25/u-s-mining-push-faces-workforce-shortage/

Visual Capitalist, Mapped: Top Destinations for Chinese Exports in 2025

https://www.visualcapitalist.com/mapped-top-destinations-for-chinese-exports-in-2025/

Inside China / Business is a reader-supported publication. To receive new posts and support my work, consider becoming a free or paid subscriber.

From Inside China / Business via This RSS Feed.